Assessing the council tax against the principles of "good" tax policymaking

This briefing presents the findings of research undertaken as part of an Academic Fellowship based in the Scottish Parliament Information Centre (SPICe) between June and November 2025. It explores how the council tax aligns with the six principles of Scottish tax policymaking, set out in the Scottish Government's 2021 Framework for Tax. Any views expressed are those of the author or interview participants.

Summary

This briefing presents the findings of research undertaken as part of an Academic Fellowship based in the Scottish Parliament Information Centre (SPICe) between June and November 2025. In this research, Dr Lewis Forsyth (University of Glasgow) explored how the council tax aligns with the six principles of Scottish tax policymaking, set out in the Framework for Tax 2021.

The research found that whilst there was indeed alignment with some of the principles, namely efficiency, certainty, and convenience, significant work was required to bring the council tax into alignment with the principles of proportionality, engagement, and effectiveness. Given that the council tax is uniquely placed to improve the overall alignment of the tax system, it is significantly underutilised in realising the Scottish Government’s tax vision.

Any views expressed in this briefing are those of the author or interview participants.

Introduction

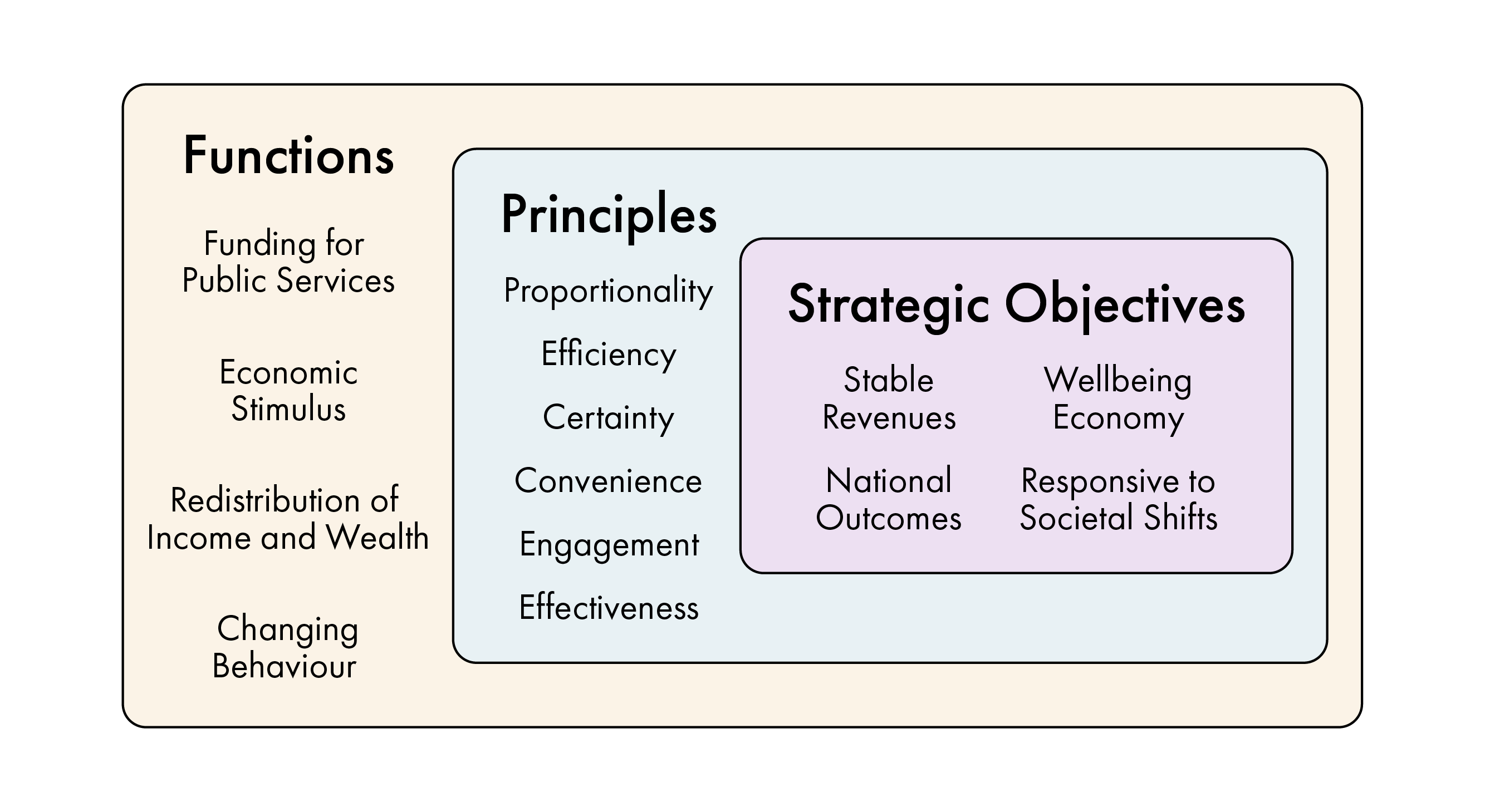

In 2021, the Scottish Government published its Framework for Tax, formalising a 'Scottish Approach to Taxation'. The document, which presents a single framework for tax policymaking and revenue raising powers in Scotland, aims to exemplify best practice and provide a “forward-thinking” approach to tax policy across all levels of government. This framework is the first of its kind in Scotland. At the core of the document are six principles which are intended to guide Scotland's approach to taxation:

These six principles reflect what the Scottish Government identify as “prominent attributes of good tax policy design”, drawn from a “set of values that can be identified in international good practice and tax policy literature”. These principles are neither mutually exclusive nor collectively exhaustive, but they are clearly identified as a “basis against which to assess tax policy and promote system-wide coherence”. Taken with the Scottish Government's view of the functions and strategic priorities of taxation, they aim to form a "coherent approach to tax policy”.

In this spirit, this research uses the Scottish Government's framework to assess council tax and its role in the wider tax system.

Background to council tax

Council tax is a devolved local tax which raised approximately £3 billion in revenues for local government in 2024-25. It is a banded property tax based on the value of a property in 1991, when the last general revaluation took place. In Scotland, a property's value falls into one of eight bands from A-H, with A being the lowest and H being the highest. Each year, councils set the Band D rate, with Scotland-wide multipliers applied for bands A-C and E-H. For lower value properties (A-C), the effect of this multiplier is to lower their overall bill compared to Band D, whilst for higher value properties (E-H) their tax bill is higher relative to Band D. This is illustrated in Table 1 using the fictional council of “West Muirshire”, whose Band D rate and band composition is given as the Scottish average for 2025-26. For illustrative purposes, the average increase in bill is modelled if “West Muirshire” were to increase the Band D rate in 2026-27 by 5%.

| Value Range(1991) | Band | % of Dwellings | Charge in 2025-26 | Multiplier | % of Band D | Illustrative charge in 2026-27 based on 5% increase |

| Up to £27,000 | A | 19% | £1,033.81 | 6/9 | 67% | £1,081.10 |

| 27,001 – 35,000 | B | 22% | £1,203.54 | 7/9 | 78% | £1,260.11 |

| £35,001 – 45,000 | C | 16% | £1,373.27 | 8/9 | 89% | £1,440.13 |

| £45,001 – 58,000 | D | 14% | £1,543 | 9/9 | 100% | £1,620.15 |

| £58,001 – 80,000 | E | 14% | £2,021.33 | 473/360 | 131% | £2,128.70 |

| £80,001 – 106,000 | F | 8% | £2,515.09 | 585/360 | 163% | £2,632.74 |

| £106,001 – 212,00 | G | 5% | £3,024.28 | 705/360 | 196% | £3,172.79 |

| £212,001 or more | H | <1% | £3,780.35 | 882/360 | 245% | £3,969.37 |

We can see that increasing Band D by 5% means a household in Band A will end up paying £48 more per year in 2026-27 whilst a Band H household will pay an extra £189.

For local authorities, council tax is a key piece of financial machinery, providing some degree of fiscal autonomy and flexibility whilst strengthening local democracy by providing an accountability mechanism to their electorate. For the Scottish Government, the salience of the council tax, its role in public finances, and its potential to deliver national strategic priorities means that central government has a justifiable interest in its performance.

Council tax has long been acknowledged as a fundamentally flawed system (see Commission on Local Tax Reform, 2015), with successive governments in both Scotland and the UK consistently recognising the need for reform. This is laid out explicitly in the 2021 framework where reform of the council tax is viewed as a priority within the context of the guiding principles:

We are committed to reforming council tax to make it fairer, working with the Scottish Green Party and COSLA to oversee the development of effective deliberative engagement on sources of local government funding, including council tax, that will culminate in a Citizens’ Assembly

The Scottish Government has just finished consulting on proposed changes to council tax, while the 2026-27 Budget includes separate proposals for two additional bands for the highest value properties. There has been no Citizens Assembly. Similar efforts at the close of Session 4 of the Scottish Parliament, through the Commission on Local Tax Reform in 2016, produced only modest changes.

Research methodology

The existence of the Framework for Tax may prove to be an important yardstick which was lacking in previous attempts at reform. It is therefore worthwhile revisiting the council tax to explore the extent of its alignment with the ‘Scottish Approach to Taxation’.

This project was completed over 6 months on a part-time basis and draws on stakeholder interviews alongside a desk-based review of relevant evidence and government publications. An initial review of material informed the interview structure, whilst desk-based research and documentary analysis were ongoing throughout the project.

Desk-based review

The evidence and policy review began with tracing the principles from their first expression in a Revenue Scotland Framework in 2015, through to their formalisation in the Framework for Tax (2021) to their most current form in Scotland's Tax Strategy: Building on our Tax Principles(2024). This was followed by an examination of the publications from the Joint Working Group on local government finance sources and council tax reform from 2022 to 2025 as well as a selection of relevant outputs from the Local Government Housing and Planning Committee. Subsequent research drew on national and international literature to supplement the findings.

Interviews

Fourteen interview sessions were carried out with 15 participants selected purposively for their expertise on council tax. This included a range of respondents from local government, Scottish Government, the third sector, and academia. Balance was sought across the diversity of local authorities to ensure both an urban and rural perspective. The research did not seek views from elected members.

Interviews were structured around a ‘report card’ where the description for each Scottish taxation principle was read to the participant who was then asked to reflect on how well the council tax was aligned. Additional questions captured views on the trade-offs between principles, which were being prioritised, where there was evidence of misalignment, and what would be needed to encourage greater alignment. Input was also sought on the principles themselves, the framework as a concept, and where there was space for best-practice learning. Interviews were conducted under the guarantee of anonymity and as such names have been removed to protect identities. The identifiers used are provided in Table 2.

| Participant | Number | Identifier |

| Scottish Government Official | 1 | Scottish Government Official |

| Local Government Finance Practitioner | 4 | Local Government Representative |

| Local Authority Chief Executive Officer | 2 | Local Government Representative |

| Third Sector Expert | 6 | Third Sector Expert |

| UK Parliamentary Official | 1 | UK Parliamentary Official |

| Academic Expert | 1 | Academic Expert |

Headline findings from each of the six principles are explored below in the order presented in the 2021 Framework for Tax document, with a ‘snapshot’ from their report card capturing some participants' immediate responses.

Proportionality

“Taxes should be levied in proportion to taxpayers’ ability to pay. The Scottish Government also believes that a fair tax system should be progressive, i.e. that the proportion of tax paid should reflect the relative income or wealth of the taxpayer. Equally, comparable circumstances should attract comparable tax treatment, in the absence of strong justification to the contrary.”

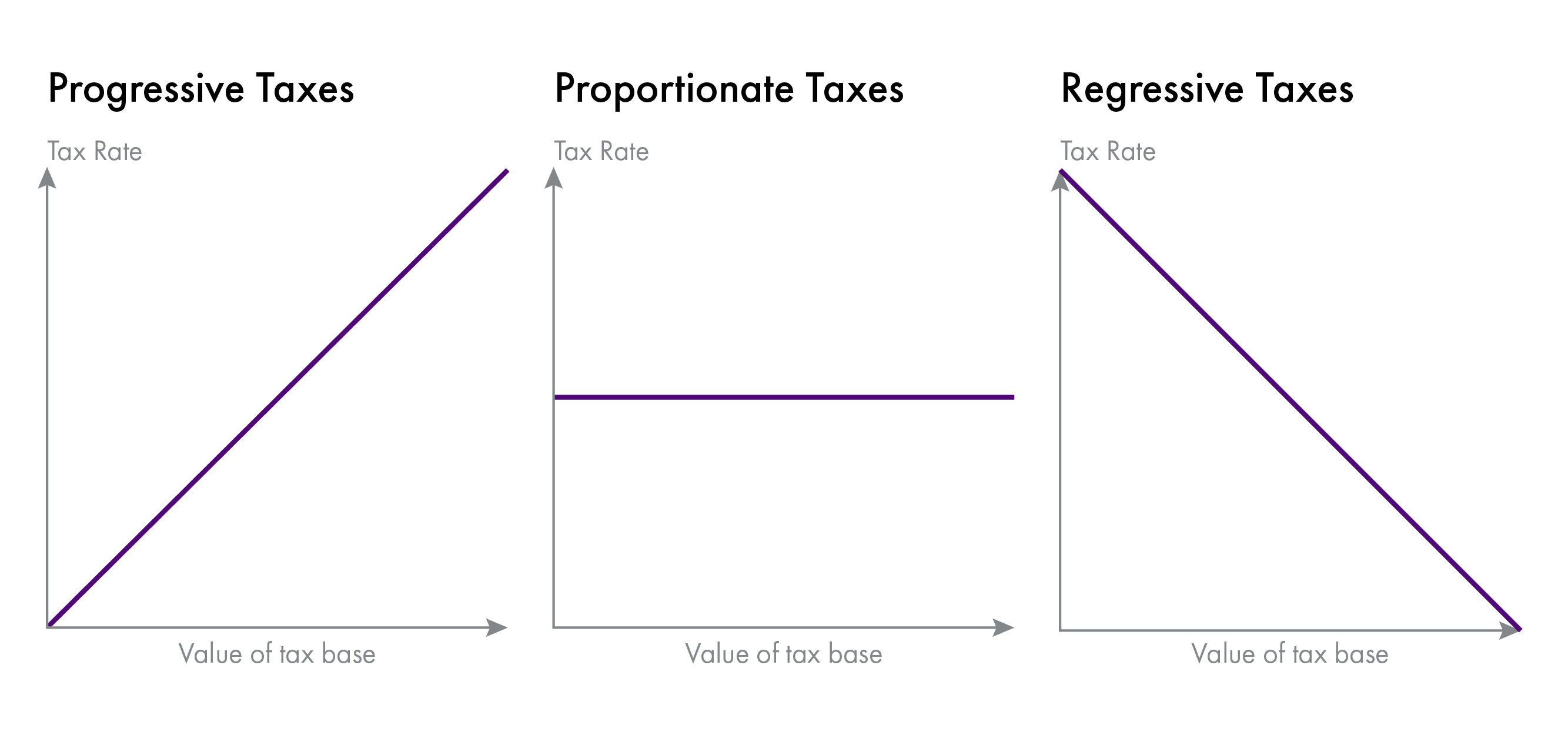

Proportional to what?

The construction of this principle is somewhat misleading. Chart 2 illustrates what is meant by proportionate and progressive taxation in economic terms, highlighting that these are distinct approaches to taxation. What is actually being conveyed by the term proportionality in this context may be better thought of as "fairness" .

The pursuit of fairness has long been an important dimension of tax design (see See Ch.4 of the Layfield Committee’s Report, 1976), however fairness is itself a contested concept and has been the subject of much debate in tax policymaking. Central to this debate is that fairness is in the eye of the beholder, and is dependent on subjective experience, values, and informationi. Typically, a “fair” tax has often been understood as one that reflects an individual's ability to pay, often measured through income, wealth, or some combination of both.

Historically, property has been treated as a proxy for both wealth and income and therefore one's ability to pay. Participants stressed that, before reliefs, the council tax does not really consider income at all as it relies exclusively on property values. The assumption that these property values somehow reflect occupants’ income was widely challenged (see Commission on Local Tax Reform, 2015). While lower‑income households often live in lower‑value properties (and vice versa), this relationship was described as rudimentary at best and certainly not universal. The classic example which disproves this link is of a retiree who has paid off the mortgage on their home, purchased on a higher income, but who now draws a more modest pension. This ‘asset rich, cash poor’ problem illustrates how difficult it is for a single property-based tax to track both dimensions of ability to pay simultaneously.

Some participants also emphasised that council tax’s relationship to wealth is also largely symbolic. Property remains only a rough proxy for wealth, ignoring savings, pensions, financial assets and business holdings. Whilst owning a property reflects a substantial asset which could be used to tax wealth, the design of the council tax means that it “is only very, very, very vaguely related [to taxing wealth] and, of course, very imperfectly because of the 1991 values” (Academic expert). Three well recognised factors were identified which cause this:

Banding weakens the link between property value and wealth. Because each band covers a wide value range, tax no longer scales with actual property values, and the top band (H) groups all homes above £212,000 together meaning properties just above the threshold are liable for the same amount as those worth several million.

The absence of revaluations compounds this, as 1991 values no longer reflect current patterns of property value across Scotland.

Band multipliers do not match real differences in property values. Band H households pay only three times as much as those in Band A, despite some Band H homes being worth ten times more.

The research heard that these features weaken the relationship between property and wealth. Moreover, these features also mean that the council tax fails on the test of progressivity which is an important amendment to this principle. Rather, council tax is widely recognised as regressive (see IFS, 2025) against property values and against income groups over the lowest 20% (a group largely protected by the Council Tax Reduction Scheme). These design choices were viewed as fundamental rather than incidental:

It's the opposite [of progressive] - it's regressive. It is in its design and how the multipliers were designed… it's in its DNA that it was never meant to be proportional or progressive.

Third Sector expert

The consensus view of those interviewed was that in its base form, the council tax is “not the most progressive, not even close to it” (Third Sector expert). The research heard that if a local tax had been designed from the first principles set out in this document, particularly the principle of proportionality, then it would not produce the council tax.

Horizontal equity

The above discussion of progressivity considered how council tax performs on vertical equity i.e. the view that those with greater income or wealth should contribute more. Horizontal equity requires that people in similar circumstances pay similar amounts; in principle, a household in Shetland should therefore pay the same as one in Shotts, all else being equal. The proportionality principle touches on both dimensions. However, many of the features that weaken vertical equity (noted above), particularly banding and the absence of revaluation, also undermine horizontal equity. One Expert highlighted this challenge:

Firstly, the fact it hasn't been revalued for 35 years means you have properties that were worth the same in 1991 but are now worth hundreds or thousands of pounds different, still facing the same tax rate. Conversely, [two properties] now worth the same face bills hundreds and hundreds of pounds a year different because they used to be worth different amounts back in back in 1991.

Property values have changed significantly across the country, as the recent consultation from the Scottish Government confirms. Analysis by the Institute for Fiscal Studies indicates that while average property values are estimated to have increased by 357% since 1993, there has been significant variation across Scotland. Aberdeen City has seen below average rises of 168%, whilst high demand areas like East Lothian have seen increases of 500%. Such are the variations that the average property value in Edinburgh (£335,000) is over twice the average property value in East Ayrshire (£141,000).

Horizontal equity is further undermined by the use of broad property bands. While banding brings simplicity and reduces the likelihood of appeals, its weaknesses have been magnified by the lack of revaluation. As property values have shifted, many homes now sit in outdated bands. Evidence from the Institute for Fiscal Studies and the Commission on Local Tax Reform suggests that roughly as many properties would move up a band as down in a pure revaluation. Regardless of direction, any property in the wrong band fails the test of proportionality. This illustrates how design choices, such as on banding and revaluation, have not only created but entrenched inequity.

A further issue which interviewees said jeopardised this principle was the council tax freeze. First introduced through the 2007 Concordat between the Scottish Government and COSLA, the freeze compensated councils for lost revenue through additional central grant funding. Because the freeze applied uniformly across all bands, the highest‑value households received the largest cash‑value savings as a 3% saving in Band H is far greater in cash terms than a 3% saving in Band A. Although lower‑income households may have gained more in relative terms, many Band A, B and C households already receive Council Tax Reduction (CTR). As a result, those on the lowest incomes were largely protected from the outset and saw little additional benefit. These effects are well documented, such as by the Fraser of Allander Institute and the Institute for Public Policy Research (IPPR) whose analysis shows that even after accounting for the CTR scheme, cash savings rise across the income distribution, with the wealthiest 10% of household saving more than twice as much as the lowest.

It is also worthwhile restating in plain terms the logic of funding a freeze with central transfers. Revenues generated from more progressive national tax sources are being used to subsidise a largely regressive property tax, the consequence of which being to make it more regressive. This is contradictory to the aims of system-wide proportionality.

Council Tax Reduction Scheme

A number of features were identified which have made council tax more progressive or ‘fair’ over time. The primary means by which council tax is made more progressive is through the Council Tax Reduction (CTR) Scheme. The research heard a range of positive comments relating to the CTR Scheme, particularly as they relate to Scotland, and the benefits these have had for ensuring better alignment with the principle of proportionality.

Offered on a means tested basis, CTR provides reductions of up to 100% on council tax bills for those on low incomes in Scotland. As of November 2025, over 457,000 recipients (which can be a single person or a couple, with or without children) are in receipt of some level of reduction (see Scottish Government, 2026). The CTR Scheme was introduced by the Scottish Government in 2013 to replace the abolished ‘Council Tax Benefit’ (CTB) scheme which was operated at a UK-level by the Department of Work and Pensions.

Whilst the scheme is managed locally, CTR operates at a national level with uniform rules across all 32 local authorities. This contrasts with England, where local authorities design their own Council Tax Support (CTS) schemes, without the same national consistency. The research heard that the uniform approach in Scotland, and having the scheme fully funded, was an important policy decision which had ensured greater proportionality, especially when compared to the more patchwork model in England. The effect has been that, when compared to England, there is broader and more consistent support in Scotland for those on the lowest incomes (interviews and IFS, 2019).

The CTR scheme is not without its challenges. One challenge identified was that it relies on the individual’s understanding of the tax and their entitlement to the reduction. Whilst a number of participants noted the positive work taking place at a local level, reflected in the improving take-up rate, the ongoing challenge of underutilisation was raised throughout discussions in reference to both CTR and discounts more broadly:

Unless you know about these things, you're not going to look for them. I think in terms of understanding council tax, it's not so much the basic charge itself, but it's all those discounts and exemptions without which it can be very unfair.

Third Sector expert

Given that the fairness of council tax is so dependent on exemptions, discounts, and reductions, the efficient operation of this system is extremely important in ensuring adherence to proportionality. Despite its limitations, the Council Tax Reduction Scheme remains the most significant mechanism for improving proportionality and offers the strongest opportunity to align the tax more closely with this principle.

Efficiency

“The tax system must balance the prospects for revenue against the potential for unintended behavioural responses. If such responses reduce economic activity… they can create economic inefficiencies.”

Economic theory holds that property taxes can generate both intended and unintended effects, with good tax design seeking to minimise the latter. In principle, property taxes can influence decisions about buying, selling, or altering properties. In practice, participants in the report card exercise felt that council tax performs reasonably well on efficiency, since the tax can be relatively small as a fraction of overall housing costs (in the short term) and is recurrent rather than transactional. Although inefficiencies and distortions exist, most agreed these are limited in scale, especially as compared to Land and Building Transactions Tax (LBTT). Concerns about efficiency were directed mainly at discounts and levies rather than at the core design of the tax.

When the council tax was designed in 1991, debates which had informed the previous Community Charge ("Poll Tax") relating to what a property tax should do, who should be liable, and how to produce a tax which reflects an individual’s consumption on local services remained. In finding a compromise between the old Domestic Rates system, and the ‘personal’ focus of the Poll Tax, a distinctive feature of council tax is the provision of a 25% discount for households where only one adult resides in the property. A Third Sector expert explained:

If it was a [true] property tax you wouldn't have that discount because the property value is the same whoever lives there, it's a hangover from thinking about it as a charge for services.

This produces contradictory incentives for those living alone in properties too large for their needs as they are arguably being subsidised to do so. As it is a percentage discount, this also means that the higher the band the single person is in, the greater the cash discount they receive. For instance, the 2024/25 discount available in the average Band H property is approximately £870, whereas for a Band A property the cash discount is only £237. This sends confusing price signals to taxpayers. A potential solution was offered by one Third Sector expert which would make the discount structure far more progressive whilst maintaining the discount itself:

If you wanted to, you could still give a discount like that in a way that didn't distort behaviour. Rather than make it a percentage of the bill, it's a flat cash amount the equivalent of 25% of a Band A property… It'd actually be more progressive because poorer single people tend to live in the lower band properties and get a potentially bigger discount but it's not distorting property choice.

Returning to the above example, both a Band A and Band H property would therefore receive a discount of £237. If the rationale for having a single person discount is that they place less of a burden on services, then such an approach is more coherent in theory since property value is not proportionately linked to local services, nor does the cost difference between one-adult and two-adult use of services scale with property value.

A key issue which has compounded inefficiencies, as it has with proportionality, relates to the valuation lists. An academic expert explains:

The inefficiency of council tax is the lack of accuracy of the valuation… lots of properties we believe are in the wrong bands so that's having an unintended consequence in the sense that it's meant to be a tax on property but it's actually not accurate. So that has consequences on people's economic decision making - affordability, cost of living, etcetera.

Moreover, in organising the valuation at a national level in 1991, regional variations have been ‘baked in’ and amplified since, where areas of broadly higher value have lower tax rates and conversely areas of lower value have higher tax rates. Whilst this effect is especially pronounced in England, where the differences in property prices are more extreme than in Scotland, the gap between average property prices is growing steadily across Scotland as well. The resulting spatial unfairness “is just totally perverse and impacts on people's economic decision making” according to one academic expert (See also IPPR: A Wealth of Difference (2018)).

Theory vs Practise

The general sentiment across the interviews however was that council tax and its various augmentations had a weaker influence on behaviour than might be otherwise assumed from the economic theory. Often, this was contrasted against the Land and Buildings Transaction Tax (LBTT) which was viewed as more clearly affecting economic decision-making and creating distortionsi. Whilst most acknowledged that it could affect the choice to buy, sell, or rent a home, this was likely overstated. A number of reasons were provided for this. A local government representative suggests that the sums involved were ultimately not great enough to make a substantial difference:

I doubt that council tax level is a big factor in making a decision about where you live or whether you move… unless you're making a very different change in your life, you're unlikely to be moving very much between bands. You know, maybe one or two, [maybe] three bands, depending on the Council area that you're moving to. I don't think the sums involved would be sufficient to make that a big [factor].

This was echoed by a third sector expert, who raised the LBTT point:

Whether you're buying or changing where you're renting, you will look at what band it is, but it's probably not going to be a decisive factor… it's not like the Land and Building Transaction Tax that might make someone say ‘actually we're just going to stay here and build an extension rather than move house’ … I don't think it's got significant unintended consequences like that.

They went on to explain that compared to LBTT, which is a significant one-off payment for those buying a property, council tax is not only paid by a much broader section of the population, but it’s also a recurring and (in the short term) much smaller cost to factor into the immediate decision. Additionally, the research heard that the shared burden of council tax, in that all households not exempt make some contribution, makes its payment more palatable. One expert added that, at best, it might encourage some to game the system by “declaring a [second] property now belongs to somebody else” but that this is “at the margins” and likely only impacts the wealthiest.

Certainty

“Taxpayers must know if they are liable to pay tax, the amount to be paid and when it is to be paid. This allows businesses and individuals to plan and invest with confidence. Changes to the tax system should be justified and, where possible, follow a predictable fiscal cycle or published roadmap.”

Snapshots from the report card above reflect the generally positive view that most had when it came to council tax’s alignment with the principle of certainty. In the first instance, most agreed that it was clear who was liable to pay for it, largely since it was “one of, if not the most, visible taxes on households” according to one official. This meant that people generally understood the tax and their responsibility as taxpayers, even if they were less clear on how it connected to the broader system of local government finance. There was also broad recognition of the system in general terms, as well as clarity about the specific amount individuals were required to pay:

I think people are aware of it, and aware that they have to pay it, and are aware of what that charge is.

Scottish Government official

While it was felt that public understanding was strong overall, the research heard that this was more limited when it came to discounts and exemptions. Nevertheless, the tax was generally regarded as providing in‑year certainty for taxpayers:

They know that once [the bill] is sent, that's the value. That's what they're going to pay. It's not going to change during the course of a year, which I think is helpful.

Local Government representative

These features also provide a measure of certainty for local authorities. A property-based local tax is widely recognised as a stable and reliable source of revenue because such assets are difficult to conceal, and changes to the tax base, such as new housing developments or demographic shifts, occur gradually and with advance notice. One academic expert described immovable property as a far more “robust” tax base than income, spending, or individuals (as seen with the former "Poll Tax"). This stability explains why property and land taxes are used to some extent by all OECD countries: they are straightforward, predictable, and offer confidence for public finances.

While this short-term predictability was welcomed, interviewees stressed that it does not guarantee certainty over the medium or long term. Some pointed to unresolved political questions, like the prospect of reform or revaluation, as the greatest source of uncertainty. Others argued that a property-based tax like council tax cannot easily respond to economic fluctuations or unforeseen events. A broader view suggested that persistent pressures on public finances make true certainty impossible.

Council Tax Freeze

Whilst the council tax has a solid basis to align with this principle, the frequent, and sometimes unexpected, use of council tax freezes in Scotland has created uncertainty for both taxpayers and local authorities.

Interviewees described a “will they/won’t they” question which hung over the tax and made it difficult to plan for the future. The annual budget-setting cycle, combined with ad hoc freezes or sharp increases, compounds this unpredictability. One respondent framed the situation as a ‘lose-lose-lose’ scenario:

So if you're an individual and you're trying to plan your budget for next year, you don't actually know whether the council tax is going to be frozen or not. And you don't really have any idea, if it isn't going to be frozen, how much it's going to go up by until the council's pass their budget… you don't see the same thing in other taxes - it would be very surprising to imagine a 15% increase in any other tax.

Third Sector expert

This volatility is the product of a vicious cycle: frequent freezes lead to steeper hikes when they end, which in turn makes freezes more politically attractive. As one participant explained:

It's a perfect storm in Scotland because it basically means that council tax is frozen quite a lot of the time and then whenever it's not frozen it’s really jumped… and [this] increases the political capital that can be gained by freezing it [again] because you can say, ‘oh, I've saved you from a 12% jump or whatever this year’ .

Third Sector expert

While the principle focuses on certainty for taxpayers, interviewees stressed that this volatility affects everyone involved. It destabilises public finances and undermines democratic principles by stripping local authorities of their primary fiscal lever and their ability to ‘scenario test’ and respond to local priorities.

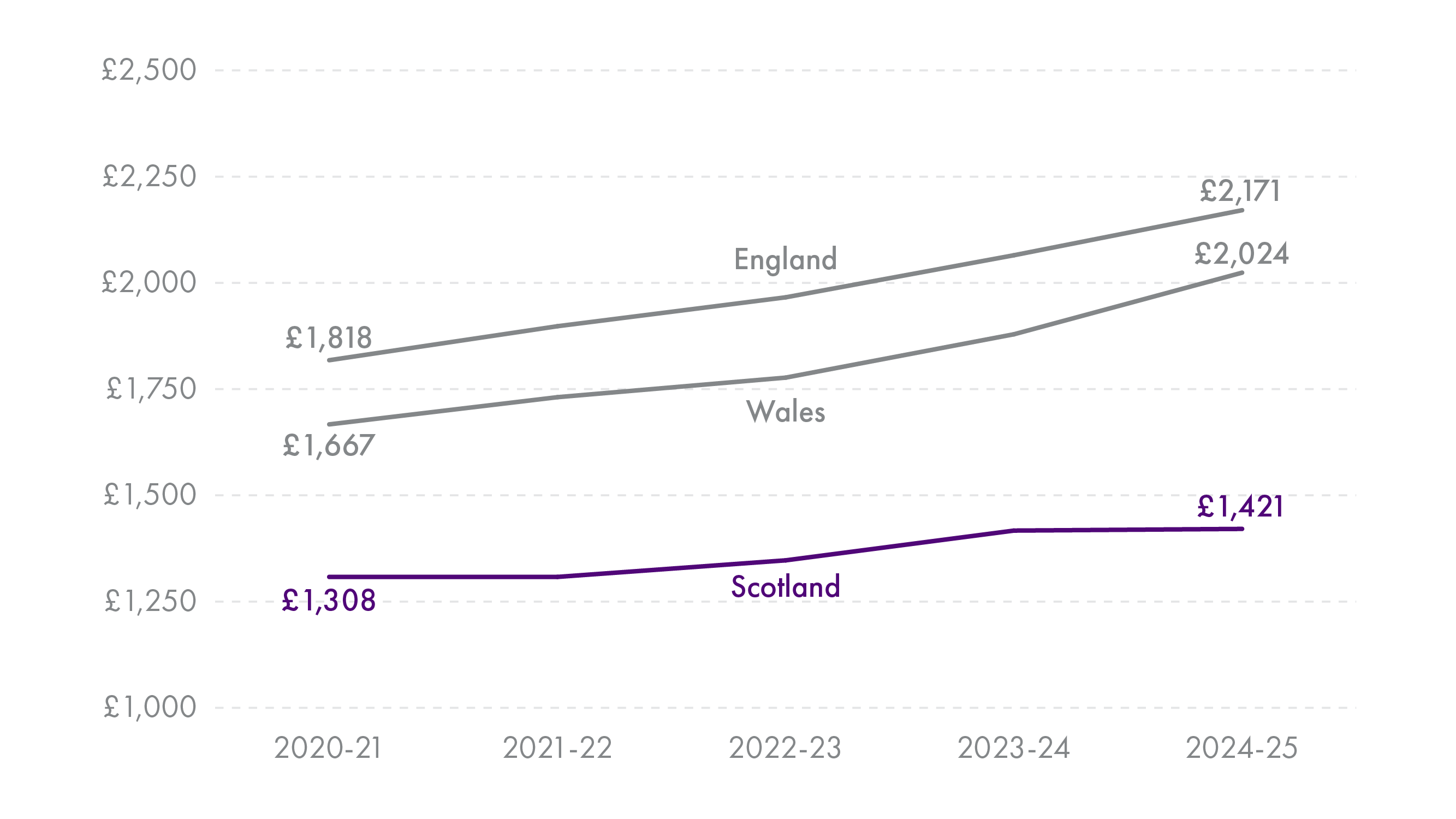

Furthermore, because council tax is a recurrent tax, any increase becomes part of the baseline and raises yield in every subsequent year. A freeze therefore forgoes this compounding effect. This results in a lasting dampening of local authority council tax revenue growth. The effects of this are that the average council tax bill for Band D is now lower in real terms than it was in 1999.

Chart 3 shows that the average Band D council tax bill in Scotland is considerably lower than in England and Wales today. Whilst this may be good news for Scottish taxpayers, council tax freezes have had significant effects on local tax revenues and broader public finances.

The Scottish Government includes the following caveat to council tax comparisons:

“Approaches to Council Tax differ across the nations, so full coherence is not possible and caution should be taken when making statistical comparisons. Property prices differ across the nations and have diverged since the 1991 valuations. The Council Tax bill in England contains additional elements, and special factors are taken into account when setting Council Tax levels. Properties in Wales have undergone a more recent revaluation than the other nations, and there will usually be other authorities levying Council Tax in addition to local councils. These are all factors which are likely to affect comparability in the statistics.”

Convenience

“Taxes should be collected at a time and in a manner that maximises convenience for taxpayers. Tax policy should be as simple, clear and straightforward as possible and opportunities to streamline the tax system should be taken where they arise.”

Convenience also stands out as a principle which the council tax largely meets. Conversations highlighted that the flexibility in payment options means that its relatively easy for the taxpayer to meet their obligations, however it is not as convenient as other taxes within the system such as Value Added Tax (VAT) or Income Tax. This provoked a number of conversations about what degree of convenience was appropriate for a tax which is so fundamental to the democratic link between taxpayers and local authorities.

Whilst a minority choose to pay their council tax in a single instalment, the vast majority pay monthly and an increasing number do so via direct debits. Traditionally, council tax instalments have been paid over 10 months, but all Scottish councils now offer the ability to pay over 12 months via standing order. Whilst some reflected that many “quite like the two months they get off” on the classic 10-month option, being that it provided a welcome respite for some over February and March, it may have also caused unnecessary problems for others:

I think the move to make 12 months rather than 10 months the default is helpful because for those that don't pay by direct debit, the two months gap you weren't paying was causing some issues. Some people might pay in that period when they didn't need to. Others might then forget when it comes to April that they need to start paying again.

Third Sector expert

For those paying over 12 months, the regular schedule creates a predictable routine, supported by the assurance that bills will remain unchanged during the year unless personal circumstances shift. This arrangement enhances convenience for taxpayers and improves certainty for local authorities by sustaining high collection rates.

Where concerns about convenience arose, they were typically in comparison to highly streamlined taxes such as VAT (largely embedded in the price of goods and services) and income tax (deducted automatically from wages). Yet most agreed that in terms of a locally delivered tax, it would be hard to imagine it being significantly more convenient. The main exception related to the Council Tax Reduction Scheme. As noted earlier, taxpayers must actively apply for discounts or exemptions, and navigating this complex system can be challenging even for those familiar with it.

Level of Convenience

One reason the council tax remains politically sensitive is its high visibility; for most households, it is a conspicuous charge that has only ever been frozen or increased in Scotland since 1999. This has meant that the council tax has historically been ‘felt’ especially hard by the taxpayers, although the trend towards direct debits may be reducing this impact. A recurring theme in the discussions was how much convenience should be built into a tax so closely tied to local democracy. Many participants argued that it should not become as ‘invisible’ as taxes like VAT or income tax, “where you don’t even think about paying it—it just happens” . One participant posed the question:

Actually, do you want taxes to be convenient? The more convenient they are, the less obvious they are, and that means people take less notice of them - so then you've got that issue of engagement and ability to understand and communicate, [and that] is maybe affected negatively by convenience.

Third Sector expert

It is both important and difficult to strike the correct balance on convenience for this reason, although interviews suggested this is not currently being managed as effectively as it could be:

I'm not saying that taxes should be invisible, but there has to be a happy medium… [Currently], you get a letter through your door that says your council, the thing that, you know, you are increasingly not getting many services from, is asking you to pay more again - that's not a recipe for high levels of public satisfaction.

Third Sector expert

Striking the right balance is crucial to ensuring that council tax remains acceptable to the public.

Engagement

“People and businesses should be able to understand the tax system and governments and tax authorities play a critical role in relation to that. Governments must therefore be open and transparent about tax policies and their decision-making, consulting as widely as possible. This is crucial for accountability and trust.”

Interviewees generally felt that the council tax was poorly aligned with the principle of engagement. They pointed to financial complexity, political manoeuvring, and a lack of clear purpose as holding back engagement efforts. A key challenge is that engagement exercises are often met with scepticism across stakeholder groups. Several participants noted that previous council tax consultations "haven’t always led to meaningful change" which led to scepticism towards any current or future efforts. There was a sentiment shared by some that engagement exercises, whether locally or nationally driven, were largely "performative" or simply “discharging an obligation". This was partially confirmed by one respondent reflecting on the local budget setting process:

To an extent it's a bit of an exercise in saying that you've engaged because they don't want to make [tough decisions]. Just like councillors don't want to make really tough decisions, neither does the public.

Furthermore, it was not necessarily clear to interviewees what the purpose of engagement exercises were at the Scottish Government level, or whether there was the conviction to deliver change. One respondent reflected that part of this problem was that consultations were effectively putting the cart before the horse:

There's a broader issue here, which I didn't quite pick up from any of the principles, which is ‘what's the balance between the different taxes that make up the tax system and what's the rationale behind that?’ Now if you're the government and you're trying to be transparent about tax policies and consult as widely as possible, it seems to me that part of that is giving an account of why you're trying to raise a certain amount of tax from one route and a certain amount of tax from another route. Why is it that council tax raises the amount that it does in Scotland, which is significantly less than it does in England?

UK Parliamentary official

Some participants noted that constant engagement exercises on council tax reform with very little change have created a ‘boy who cried wolf’ scenario that has led to public disengagement.

Along these lines, another questioned whether the current consultation might be another example of this pattern:

The complexity of the engagement… I don't anticipate you'll get many people in the community reading that and distilling that and seeing what that kind of means. I don't know if that means it's an efficient engagement and certainly the timing of it again doesn't set out that they're wholly standing behind this in terms of how this might be delivered going forward.

Local Government representative

The complexity of council tax and the wider tax system was consistently identified as a challenge in its own right, but this was particularly true for public engagement. It was noted that even experts found it difficult to engage meaningfully with the latest consultation:

I [had to] sit down and wrap a wet towel around my head as I tried to get into the detail of it… I gave up and I said that to my Chief Executive ‘this is the point at which I need to go away and have a think about it’. I suppose in terms of engagement, does this represent good engagement when you're leading with hedonic regression principles upfront ? I don't know if it's particularly understandable.

Local Government representative

Even when these barriers are not present, it can be difficult to capture views from across the population:

It's primarily middle class, older people - it's essentially non-marginalised communities and that just means you get one point of view on what's worth doing and that's where engagement can fall down is that you get the engagement of the most engaged members of any community.

Third Sector expert

Echoing this view, a Local Government representative was even more blunt: “the problem is that the local community doesn't really want to engage with you”. Challenges around engagement are not unique to Scotland or to local government finance. Successful engagement, particularly on complex issues, requires significant time and resources. A recent two day ‘citizen’s panel’ on property tax reform from the UK Collaborative Centre for Housing Evidence suggests that the public are capable of overcoming the challenges of complexity and that, when they do, many favour more radical reform. This experience also suggests that ‘unlocking’ these views requires both time and resources.

Effectiveness

“Design of the tax system should focus on ensuring taxes raise the expected revenues and achieve their intended aims. This includes designing taxes that minimise opportunities for tax avoidance. The vast majority of taxpayers want to pay the correct amount of tax, and do, but where taxpayers do engage in avoidance practices governments and tax authorities should respond quickly and proactively to tackle them.”

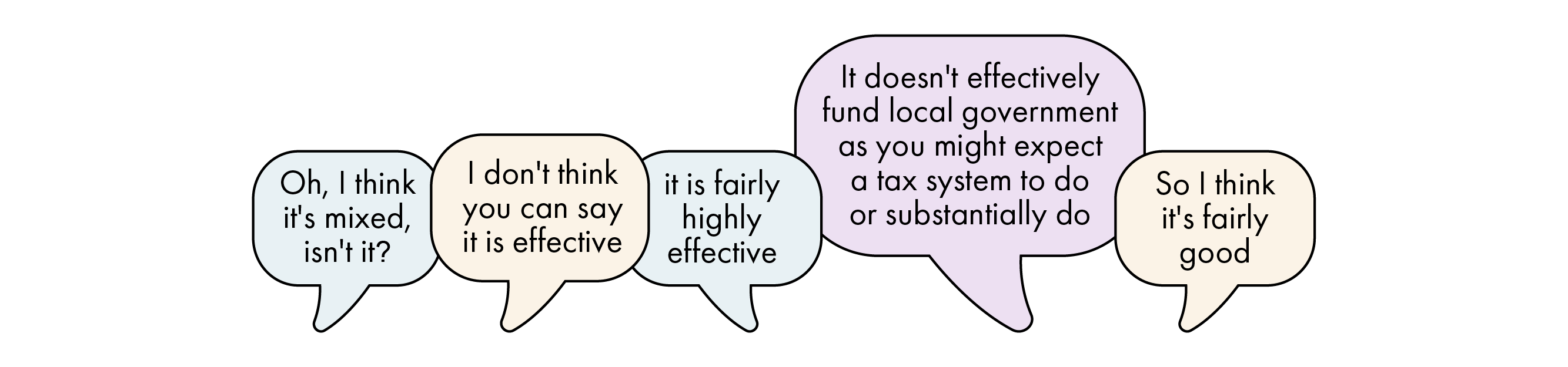

Whether or not the council tax can be considered to be an effective tax received mixed feedback, largely reflecting the two different goals set out in the description of the principle. On the one hand, there was broad agreement that the council tax was effective in raising expected revenues and that the design of the tax did indeed minimise opportunities for tax avoidance. On the other, there was a range of views as to what the intended aims of the tax actually were, what they should be, and whether they were delivering on either.

The council tax has a high collection rate reflecting the fact that it is difficult to hide property or otherwise avoid paying the tax. For the same reasons it is also highly predictable since data on the tax base is so comprehensive. This allows for fairly reliable modelling of financial scenarios and allows councillors, local authority officials and civil servants to test the effects of potential tax changes, albeit on the proviso that grant funding may impact these plans. Moreover, the theoretical tax base is nearly always growing as more properties are developed. The research heard that all these features made for an effective tax.

There were three dimensions on which it was viewed as ineffective in terms of raising revenues. The first, covered already, is that the lack of revaluations means that whilst it might raise the expected revenues from the tax base as it is currently divided, this is detached from the true reality of property prices. The second issue is that council tax provides only a modest share of local government revenue, meaning it does not adequately fund local services on its own:

Is it effective? Well it doesn't effectively fund local government, as you might expect a tax system to do or substantially do... given it is the principal means of local authorities directly levying tax, it's quite ineffective because whatever you do with it can only affect somewhere between presumably 8 and 12% of your income…

Local Government representative

Whilst this reflects one perspective on Scotland’s revenue mix, it is nonetheless the case that both the UK and, even more so Scotland, have some of the most centralised systems of local government finance, especially when looking at local taxes as a percentage of local expenditure. At best, council tax was effective as a ‘top-up’ mechanism in this view.

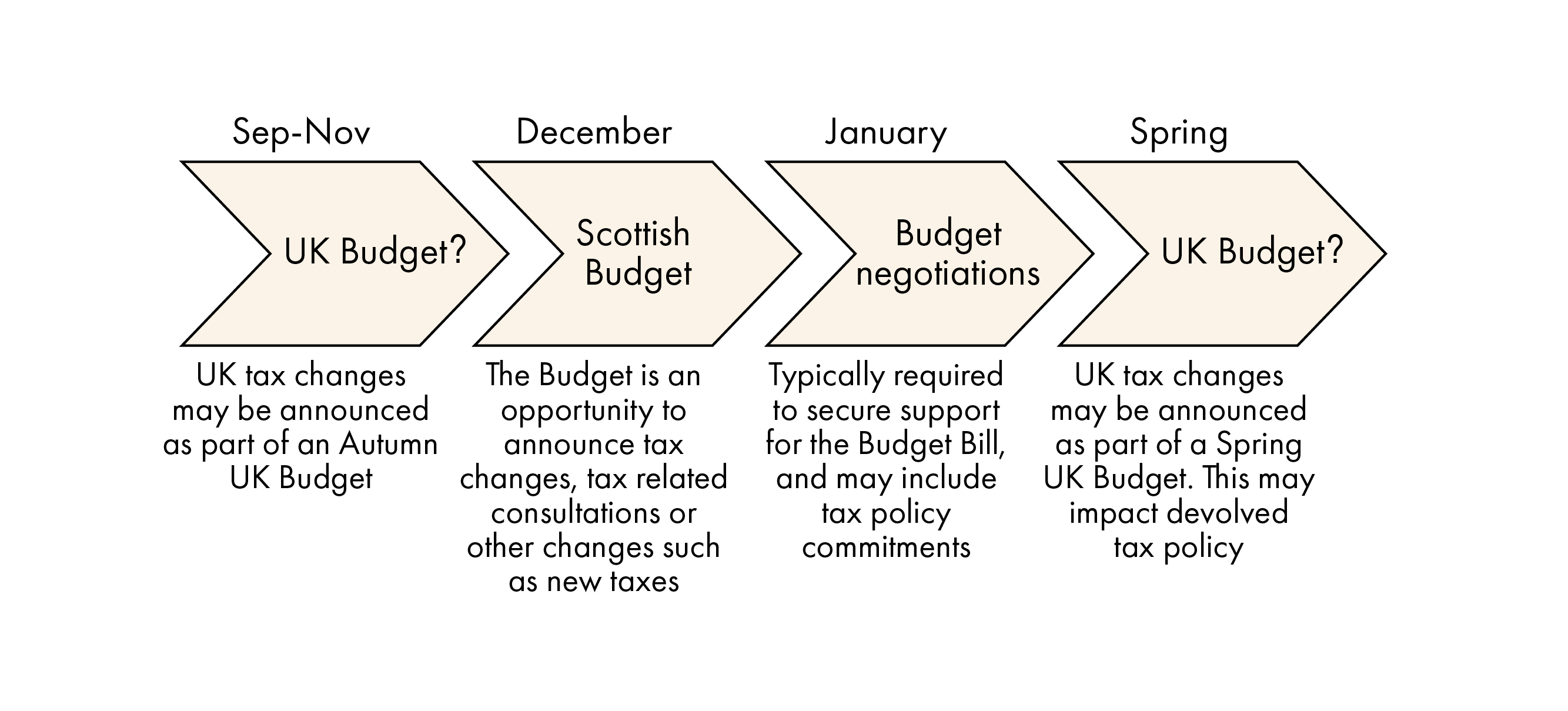

The final issue raised was that the compressed timelines which the budget setting process now runs has proved challenging for officials. This process makes it difficult to know what revenues need to be expected and what the tax rate will need to be to deliver services. One Local Government Representative explains:

Given that the UK Government's budget isn't happening till the 26th of November, and then the Scottish Government's budget's not until January, we're very much on the back foot in terms of reacting to all of that. It doesn't really give the Council a very long lead in to making what could be quite difficult decisions on services at short notice…

The standard budget process, outlined in the Framework for Tax shows how compressed the 2025/26 cycle has been. The graphic below has been reproduced from the document and illustrates this, demonstrating the knock-on effect a late UK budget can have.

The timing of the 2026-27 Scottish Budget only left councils with around two weeks to draft budget papers based on provisional allocations, a process widely viewed as ineffective, especially when compared with earlier, more predictable budget cycles.

Intended aims

The research found that there was a lack of clarity on a very basic question – "what is the aim of the council tax?" This produced a range of opinions, ranging from a purely functional interpretation of the tax as an additional revenue source, to more political interpretations centred on its potential to tax and redistribute wealth. Some questioned whether the tax has any clear intended aim or whether it ever did.

One participant suggested that council tax and its predecessors were "never designed from first principles" particularly regarding their role within the wider system. On the matter of system-wide alignment with the principles, the council tax (or a comparable property/land tax) is uniquely placed to bring the taxation system into greater alignment. Firstly, property tax could serve as a mechanism for taxing wealth, and while using property as a proxy for wealth presents challenges, it remains a stronger option than many alternatives making it an ample starting point. Secondly, it is also particularly well suited to doing so with minimal behavioural distortions to labour supply, migration, or tax avoidance as compared to, for instance, LBTT or Income Tax (Third Sector Expert).

The Framework for Tax suggests that the tax system overall should be fair, progressive, and produce minimal economic inefficiencies, and yet the council tax as a primary means by which to achieve this is relatively underutilised. Council tax could therefore be an important lever in the overall tax system to increase progressivity and, in turn, ameliorate the trade-off between efficiency and equity. One expert suggested this might be deliberate:

They've sort of left some of this unspoken because I think they realise there's a contradiction between their timidity when it comes to revaluing and reforming and their other principles around progressivity and ability to pay.

Following a similar announcement in England, the recent proposal from the Scottish Government to introduce two new bands for properties over £1 million suggests a greater willingness to use the tax for these purposes than has been seen before.

These issues reflect a long-standing challenge, going back to at least the Layfield Commission on local government finance in the 1970s, that there lacks clarity on what local government is actually for, what services it ought to perform, and what relationship it should have with central government as a result. When asked about the aims, one expert suggested:

It really depends on what you expect council tax to be able to do. If you expect it to be able to fund local services, then you have to have a strong idea about what those local services should be. And I think that's really where the confusion is coming up - there's a long, long list of things that councils do, but it's really very hard to figure out exactly what people expect councils to do and exactly what they are required by statute to do. What we expect council tax to actually be able to fund relies on us knowing what it is we're trying to fund in the first place, and that's a big open question mark in Scotland.

Third Sector expert

It remains unclear whether the Scottish Government is satisfied with the current funding balance for local government. In England, council tax often accounts for more than 40% of overall revenues, compared to approximately 20% in Scotland. Combined with the retention of Business Ratesi, some English local authorities may have as much as 80% of their revenues raised locallyii. In Scotland, these ambiguities leave council tax without a clearly defined purpose and without this clarity it is difficult to assess whether the system is effective in raising revenue. Lacking a clear sense of its objectives, it is impossible to determine whether the tax is truly "effective".

Cross Cutting Findings

The research also captured a range of views which cut across the six principles. These broadly related to public understanding of local government finance, the role that council tax has in the broader system of taxation in Scotland (and the UK), and reflections on the taxation principles as a concept. These topics produced discussion across nearly all interviews and offer an important lens to understand the exercise of tax policy design more broadly.

Public understanding

It was noted that understanding of the council tax was not a spectrum, but rather something that people were “either hyper familiar with or completely not familiar with at all”, according to one Scottish Government official. This does not stop people having strong opinions on it:

Having a conversation around the table at a pub is quite fun about council tax, because it's just something people basically don't get for very understandable reasons, but do resent, which is perfectly reasonable.

Third Sector expert

The general view was that the majority of people fell under the ‘not familiar’ category and that this was hardly surprising given the complexity, scale, and ambiguity of local government and its finances. This was also a finding shared by the Commission on Local Tax Reform.

Even for experts, local government and its financing can be incredibly difficult to understand. This is doubly true for the layperson, whether this be navigating the system of council tax discounts and exemptions, making sense of valuation, or understanding potential changes to the rate or system. This is often not helped by sensationalism in the media and misinformation online. The research also heard that there was very little understanding about what the council tax pays for. While many people associate it with visible services such as roads, waste collection, and street lighting, there is far less awareness of the full range of local responsibilities (including the most expensive – education and social care). Participants noted a general lack of knowledge about the breadth of council functions, particularly in relation to essential but less visible services such as social care and education:

I think it's inconvenient that councils are such a complicated beast, and it's inconvenient that our finances are largely impenetrable, and I think it's inconvenient as well that those services we provide to people are often those people who don't have a voice, that can't talk for themselves.

Local Government representative

This complexity has knock-on effects on how taxpayers view council tax. Indeed, the research heard that there remained a broad feeling amongst the public that council tax was a charge for services used:

There's a lot of ‘why should I have to pay more council tax because I don't use such and such a service?’ Not appreciating that council tax only supplies about 15 to 20% of a Council's whole budget. It’s not supplying all of these other services, and it isn't a charge for services. In terms of its intended aims, it isn't supposed to just be viewed as a charge for your bins being taken… it's just a general local tax to help support local services - not actually fund them entirely. I think people don't realise how much of the local Council's budget comes from central government.

This may reflect another ‘hangover’ in public attitudes from the "Poll Tax" debates of the 1980s and 1990s but a number of features of the council tax do lend themselves to this view, particularly the name, which one official described as ‘damaging’ and ‘very misleading’ since it “naturally leads residents to think that ‘council tax’ is what pays for councils, but those of us who've studied the system know that that's never been the case, or anything like the case” (UK Parliamentary Official). The misunderstanding that the public were paying for all council activity via local taxation was repeated by a number of participants. These misunderstandings are not only unhelpful, but together with the complexity of the system they cloud some of its worst failures especially in terms of fairness:

There's a big gap in both government and civil society's understanding of just how unfair the tax system is… people have very little understanding about the current system and how that's distributed… there's just a lot of confusion… and I would argue that some of that is slightly deliberate. It's a can of worms that the government doesn't really want to open, but should be because it's really important that people understand.

Third Sector expert

Whilst the same respondent praised some of the Scottish Government’s ‘plain English’ descriptions that are available to those who ask or know where to look, there is clearly a need for in- depth work beyond standard engagement to reach those currently excluded from these debates. The earlier highlighted ‘Citizen’s Panel’ approach demonstrates the potential impact of extended deliberation.

Tax System and Principles

It is important to remember that the Scottish Government’s Framework for Tax is a framework for all tax, and indeed there is emphasis throughout the document on the tax system and its alignment to the principles. Clearly, however, it would be difficult for the overall system to be aligned with the principles if each tax within it was not striving to meet as many of these principles as possible. Nevertheless, some common taxes will perform better on some principles than others. Moreover, the Scottish tax system exists within a broader UK tax system over which the Scottish Government has limited influence. For instance, consumption taxes like VAT may be proportional (that is to say, they increase in relation to consumption), but not in relation to ability to pay (in that they are regressive to income). The question therefore ought to be: what role does council tax play within the current system, and what role might it play in ensuring greater alignment overall?

There is no universal law that says that a tax, or a tax system, need be progressive. Indeed, the word ‘progressive’ is only used twice in the Scottish Government’s Framework for Tax document. Where it does appear, however, it is central to one principle and represents the only instance in which the explanation effectively alters the principle itself. Adopting such an approach comes with a number of additional considerations, as one expert put it:

If you want a progressive tax system, and this links to efficiency and effectiveness [as well] then you need to think about “how can I redistribute in a way that also has the least behavioural distortions"

To this end, property taxes are a very effective means of balancing these competing demands. In the first instance, for a tax to be progressive it must be paid by all those expected to pay it. Not only are properties difficult assets to hide but they cannot, generally, move across borders and therefore make for a very suitable tax base. As compared to other taxes, property taxes are generally favoured by economists, including those the research spoke to, for their ability to redistribute with minimal distortions. The research heard that whilst making income tax progressive was a ‘legitimate’ choice for instance, it was probably having “not-insignificant behavioural impacts” at the top end in particular (Third Sector expert). This was even more true of LBTT and its equivalents, which are well documented for their distortionary effects. Council tax could therefore be an important lever in the overall tax system to increase progressivity and, in turn, ameliorate the trade-off between efficiency and equity.

To the extent that it has been adapted in recent years, such as through the second home premium in 2024 or the change to multipliers in 2017, there were reservations shared by many that this ‘tinkering’ was not realising the full potential of the council tax to deliver greater system wide progressivity. Importantly, any changes which are made without a revaluation are ultimately based on a tax base from 1991 and therefore not a true reflection of the distribution of properties today. This does not suggest a truly proportional or progressive tax.

However, the research also reported that whilst a clear and straightforward tax system has advantages in the round, there are valid reasons why you might wish to ensure that some taxes are ‘felt’ more than others, whether these be for the purposes of encouraging a type of behaviour or to highlight the link between taxes paid and local services. Balancing individual alignment and system alignment with the principles therefore requires a clear acknowledgement of the trade-offs, and for any decisions to be communicated clearly to taxpayer.

Finally, the simple existence of principles was not viewed as sufficient on its own to make a difference, and indeed the very existence of tax principles themselves was also drawn into question. Unofficial frameworks, such as Adam Smith’s four ‘Canons of Taxation’ or the best practise set out in the Mirlees Review have clearly shaped policymakers thinking over time, yet the practise of formalising these is relatively new. This may be for good reason. Not only are many of these principles politically contingent, but tax systems are messy and complex. They change, and often grow, from year to year in unpredictable directions in response to both national and international developments. The research heard that it is easy to lose sight of principles as you move from the abstract to the every day.

It is inevitably more challenging to retroactively apply principles to a tax that has already been created, and as the above suggests, it is perhaps even more difficult to shape an entire system around said principles. By contrast, designing a new tax with a clear idea of these principles, and how it might fit into the wider tax system, presents an opportunity for greater alignment. The research heard that, if you designed a local tax from the Framework for Tax first principles, then it would certainly not look like the council tax.

Conclusion

The Framework for Tax is an ambitious document, the first of its kind in Scotland. It sets out principles for ‘good’ tax policymaking which, together with functions and strategic objectives, are to be the basis of a coherent tax system. Where the tax system previously evolved in an organic and ad hoc manner, this framework seeks to provide coherence and consistency. However, applying these principles retroactively to existing taxes poses significant challenges. Whilst the recent update to the Framework for Tax, Scotland’s Tax Strategy, is focused on building upon these principles, it is notable that in the years since it was first announced there has been no public review of the council tax against the Scottish Government's own criteria. This research has sought to assess the tax accordingly.

The research heard that council tax is misaligned with the principle of proportionality. The language of this principle presented significant challenges in its own right, but measured against either fairness or progressivity, the council tax was viewed as failing. The council tax is regressive and only faintly related to ability to pay on dimensions of both income and wealth. While the Council Tax Reduction Scheme helps mitigate some of these shortcomings, other design choices such as banding, the absence of revaluation, and repeated freezes, undermine its effects. Despite being one of the least aligned principles, interviewees noted that the property tax model which council tax is based on is uniquely placed to encourage system alignment to proportionality and is therefore underutilised.

Whilst the council tax does create a number of inefficient distortions, interviewees suggested that some of these were less pronounced in reality than in theory. Because council tax is a relatively small, recurring cost, the research heard that taxpayers paid less attention to it than LBTT . Yet this does not mean it is an efficient tax. As above, the nature of freezes, revaluations, and banding have all created unnecessary distortions, as has the single person discount. However, when it is not interfered with, the council tax is generally effective in raising the expected revenues. Therefore, council tax is neither the most efficient nor the most inefficient tax. As above, interviewees stressed that the potential for property taxes to deliver greater tax system efficiency was not being realised.

The council tax is generally well aligned with the principle of certainty. As is common to property taxes, the nature of the tax base encourages reliability and predictability. Its high visibility as an established feature of the tax system has meant that taxpayers have a good, if surface level, understanding of their role as taxpayers. These positives are particularly true within a given tax year. Uncertainty does exist in the medium and long term particularly as a result, again, of the complications surrounding banding, revaluations, and the council tax freeze. The volatility introduced by these prevents further progress towards alignment with this principle.

The Council Tax also aligns well with the principle of convenience. Whilst there remain outstanding questions about the degree of convenience which is most desirable for a local tax, particularly as they relate to local democracy and public engagement, the present system is largely effective in ensuring convenience for both taxpayers and local authorities. However, more can still be done to ensure that taxpayers are fully aware of their entitlement to discounts and exemptions.

Efforts to date have not delivered effective alignment with the principle of engagement. Interviewees noted that the quality of engagement has undermined efforts to communicate on the council tax. This has been the case whether this be in explaining how the tax works, what role it has in the broader system, or how reform should proceed. Moreover, scepticism persists regarding the purpose of engagement exercises at both national and local levels, including among those tasked with delivering them. Future attempts to engage on the council tax are likely to remain challenging whilst the tax, and its role in both local government and broader public finance, remains so complex. In-depth engagement exercises, such as citizen’s panels, may overcome these barriers as recent studies suggest.

Finally, it remains largely unclear as to whether the council tax is effective, since it remains unclear what its intended aims are. In its narrowest sense, the tax was viewed as highly effective in that it was capable of raising the revenues expected and doing so reliably. However, this effectiveness is undermined by repeated freezes, the absence of revaluations, and compressed budget timelines, all of which complicate its operation. Whether it is effective beyond this depends on what the tax is aiming to do. This deeper purpose has been lost over time. To align with this principle, a fundamental review of the philosophy underpinning local taxation is likely to be required. The choices which are made during this process will have practical consequences for the design of the tax and will require trade-offs between the principles.

Current discussions about reforming the council tax are the latest in a long list of similar attempts. Whilst some have produced modest change, they have largely failed to address the well-established problems. As is reflected in this report, many of these problems emerge from the use and design of a banded model, a lack of revaluations, and the consequences of centrally driven caps and freezes. The recent consultation, Future of Council Tax in Scotland, is seeking views on options which may address some of these issues around banding and valuation. It would also appear that tensions around council tax freezes have cooled. These represent positive steps to addressing the shortcomings of the present system.

The December 2024 update to Scotland’s Tax Strategy places particular emphasis on three core principles: engagement, effectiveness, and efficiency. The assessment in this report suggests that there is significant work which still needs to be done to clarify the aims of the council tax, work which will require both leadership and high quality engagement. Despite property tax being a powerful tool for improving efficiency across the wider tax system, and one fully within the Scottish Government’s control, council tax remains significantly underutilised. If these principles are kept in sharp focus, then the current attempts to reform may succeed where others have failed.